WORLDWIDE FREIGHT SERVICES

Email: jack@transworldcn.com

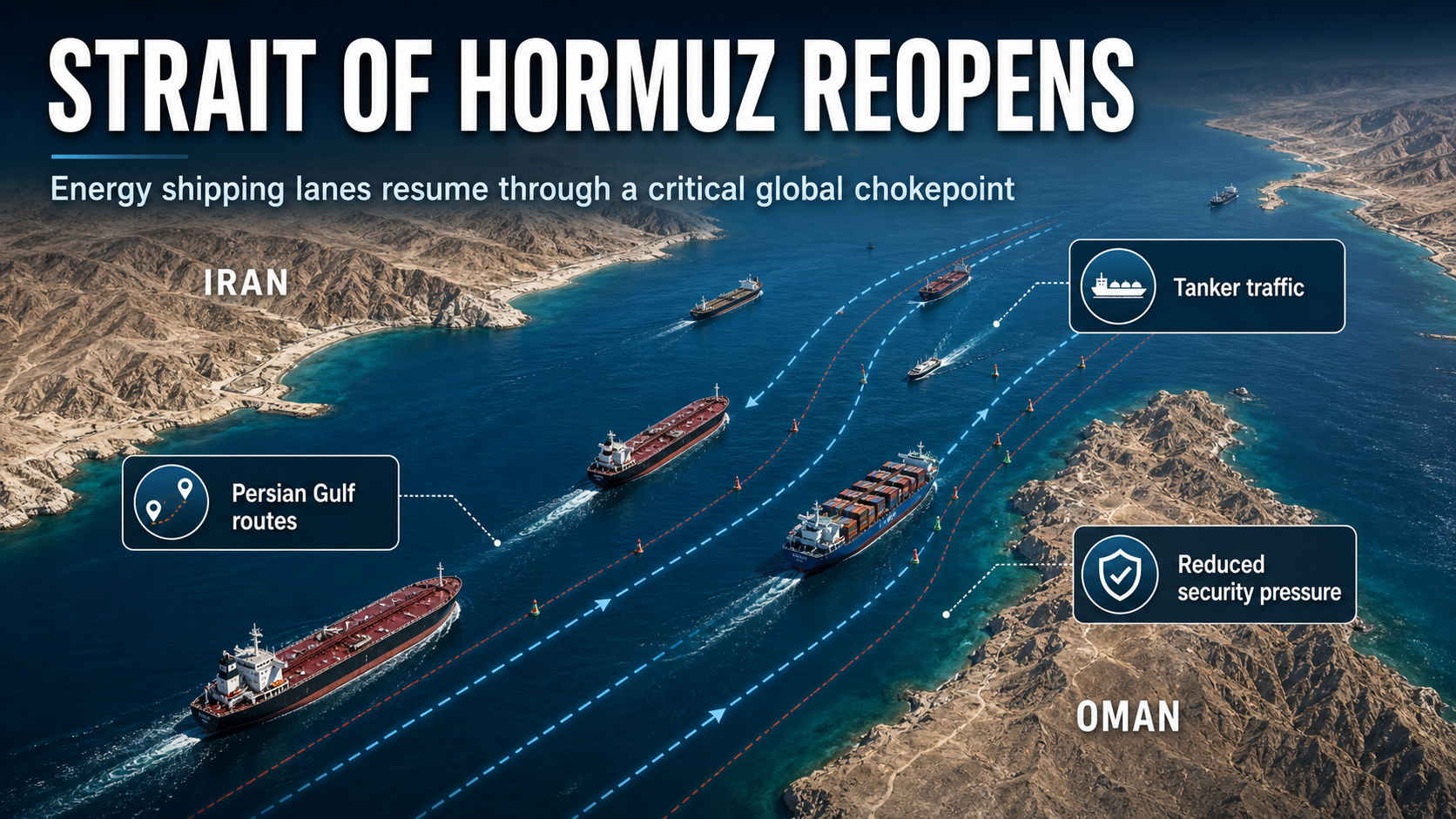

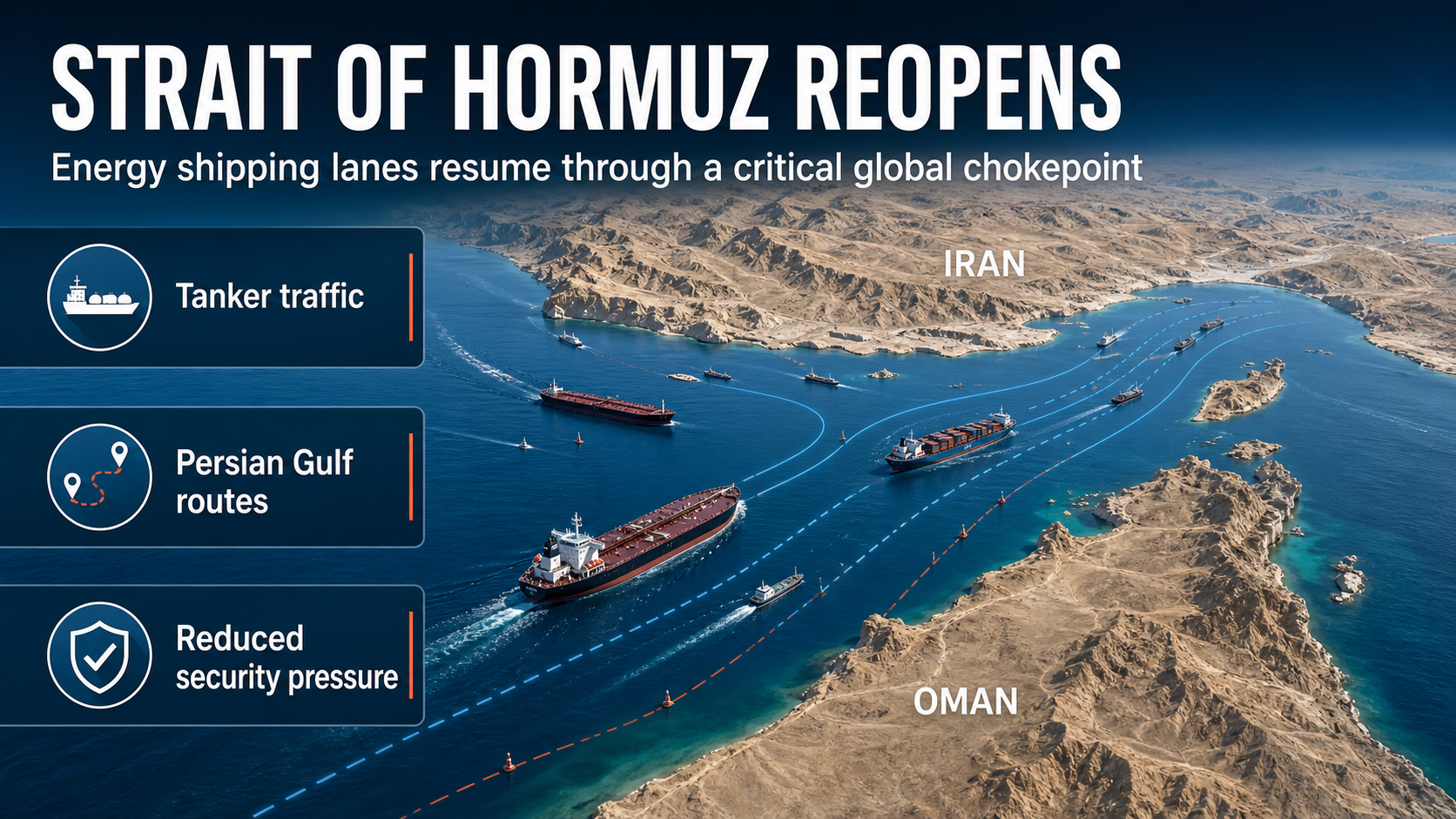

June 15, 2026, marks a pivotal turning point for global trade and logistics, as a confluence of geopolitical breakthroughs, domestic infrastructure milestones, carrier pricing actions, and commodity export surges reshapes supply chain dynamics worldwide. The most seismic development is the historic US-Iran peace agreement, which officially reopens the Strait of Hormuz—the world’s critical energy and shipping chokepoint—after months of heightened tensions and naval blockades. This decision immediately alleviates security risks for Persian Gulf routes, stabilizes oil prices, and restores normalcy to one-third of global oil shipments and a significant share of container trade.

Parallel to this geopolitical shift, China’s rail-sea intermodal transport has posted robust double-digit growth in the first five months of 2026, underscoring the country’s strategy to cut logistics costs and boost supply chain resilience. Meanwhile, leading container carriers, spearheaded by CMA CGM, have formally imposed peak season surcharges (PSS) on select Asia-Africa and Mediterranean routes, reflecting tight capacity and rising operational expenses. Finally, China’s high-value aluminium exports are experiencing a booming cycle, driven by robust overseas demand and favourable price differentials, with shipments to North America, Asia, and Mexico accelerating rapidly.

This comprehensive analysis dissects these four defining trends, exploring their root causes, immediate impacts, and long-term implications for shippers, freight forwarders, and supply chain stakeholders navigating an increasingly complex global trade landscape.

In a development that reverberated across global markets, US President Donald Trump announced on June 14, 2026, that the United States and Iran had finalized a peace memorandum of understanding (MoU), with the immediate effect of reopening the Strait of Hormuz and lifting all US naval blockades on Iranian ports. The MoU, set to be formally signed in Switzerland on June 19, 2026, mandates unfettered passage for all commercial vessels through the strategic waterway, which handles approximately 30% of global oil exports and 20% of total containerized trade prior to the 2026 tensions.

For nearly six months, the Strait of Hormuz—located between Iran and Oman, connecting the Persian Gulf to the Gulf of Oman and the Arabian Sea—was the epicenter of escalating US-Iran hostilities. Following tit-for-tat military actions, the US Navy imposed a naval blockade in early 2026, restricting Iranian oil exports and disrupting commercial shipping. This triggered a cascade of disruptions: vessel rerouting via longer, costlier alternatives like the Cape of Good Hope, 15–20% higher freight rates for Persian Gulf routes, acute shortages of oil and petrochemical products in global markets, and heightened insurance premiums for ships transiting the region.

The finalized agreement, as outlined by senior US and Iranian officials, includes the following critical provisions:

The reopening of the Strait of Hormuz delivers instant relief to global supply chains, with far-reaching consequences for multiple industries:

For shippers, particularly those in the energy, manufacturing, and retail sectors, the Hormuz reopening translates to lower costs, faster transit, and reduced supply chain uncertainty. Forwarders specializing in Middle East and European trade are already reporting increased booking volumes as clients rush to capitalize on the restored route efficiency.

While geopolitical tensions eased in the Middle East, China’s domestic intermodal logistics sector delivered strong growth in the first five months of 2026, driven by policy support, infrastructure expansion, and corporate adoption of cost-effective supply chain solutions. According to official data released by China State Railway Group (CR) on June 14, 2026, national railway freight volume reached 1.67 billion tonnes from January to May, representing a 1.8% year-on-year increase. The standout performer was rail-sea intermodal transport, which handled 7.58 million TEUs, a robust 11.0% year-on-year surge.

The double-digit expansion of rail-sea intermodal volumes stems from three core factors:

Beyond the headline 11% growth, several key metrics highlight the sector’s momentum:

For businesses engaged in China’s import and export trade, the rail-sea intermodal boom offers tangible advantages:

Forwarders are increasingly integrating rail-sea solutions into their service portfolios, with many reporting 30% growth in intermodal booking requests in 2026. As China continues to expand its multimodal network and refine regulatory policies, rail-sea transport is poised to become the default choice for cost-conscious, sustainability-focused shippers.

In a move that underscores tightening capacity and rising operational costs, CMA CGM, the world’s third-largest container carrier, officially implemented revised peak season surcharges (PSS) on June 15, 2026, for all Asia–Mediterranean and Asia–North Africa westbound routes. The French shipping giant’s decision follows similar announcements from peers including Maersk, Hapag-Lloyd, and MSC, marking a coordinated industry push to pass on higher fuel, labor, and insurance costs to shippers amid robust summer demand.

The revised surcharges represent a significant increase from CMA CGM’s initial May 25, 2026, PSS announcement, with rates as follows:

CMA CGM’s move is part of a broader industry trend, with major carriers imposing PSS on key routes in June 2026:

The coordinated PSS hikes stem from three interconnected challenges facing container carriers:

The PSS hikes add significant cost pressure to shippers, particularly small and medium-sized enterprises (SMEs) with limited pricing power. For a 40′ container shipped from Shanghai to Marseille, the combined base rate + PSS now exceeds $5,500, representing a 25% increase from Q1 2026 levels.

Forwarders are advising clients to book early, lock in rates, and explore alternative routes (e.g., Asia–Black Sea–Europe) to mitigate costs. While the Hormuz reopening may ease some pressure, carriers have signaled that PSS will remain in place until at least September 2026, as demand is expected to stay strong through the summer.

Completing the June 15, 2026, logistics landscape is the explosive growth of China’s aluminium exports, which have emerged as a bright spot in the country’s commodity trade. Driven by robust overseas demand, favourable price differentials, and Middle East supply disruptions, China’s exports of unwrought aluminium and aluminium products reached 598,000 tonnes in April 2026, a 15.4% year-on-year increase and the highest monthly level since December 2024. For the January–April 2026 period, cumulative exports hit 2.053 million tonnes, up 8.9% year-on-year.

The boom in China’s aluminium exports is fueled by four critical factors:

The surge in aluminium exports has had a direct impact on shipping and logistics:

Industry analysts remain bullish on China’s aluminium export prospects for the remainder of 2026, with full-year exports projected to reach 6 million tonnes, surpassing 2025 levels. Key risks include a potential narrowing of price differentials if global supply recovers or Chinese domestic demand rebounds, and trade protectionism (e.g., tariffs) in major markets. However, with Middle East supply uncertainty persisting and global demand for high-value aluminium products remaining strong, China’s export boom is expected to continue through Q4 2026.

June 15, 2026, stands as a defining day for global logistics and shipping, marked by transformative geopolitical, economic, and industry-specific trends. The US-Iran peace agreement reopening the Strait of Hormuz has alleviated critical supply chain risks, stabilized energy prices, and restored efficiency to one of the world’s most important shipping lanes. Domestically, China’s rail-sea intermodal sector continues its robust growth, offering shippers cost-effective, sustainable alternatives to traditional transport modes. Meanwhile, leading carriers’ imposition of peak season surcharges reflects the ongoing balance between strong demand and rising operational costs, while China’s aluminium export boom underscores the country’s role as a global supplier of high-value commodities.

For shippers, forwarders, and supply chain stakeholders, these trends demand agility, strategic planning, and adaptability. Navigating the post-Hormuz landscape requires monitoring geopolitical developments, optimizing transport modes (e.g., rail-sea intermodal), and proactively managing costs amid carrier price hikes. As global trade continues to evolve, staying informed of these interconnected trends will be critical to building resilient, efficient, and competitive supply chains in 2026 and beyond.

Email:

Email: