WORLDWIDE FREIGHT SERVICES

Email: jack@transworldcn.com

The continuous recovery of US consumer markets and low commodity inventory levels have become the core demand-side drivers of the current China-US shipping boom. After rounds of inventory destocking in 2025, retail enterprises, supermarket chains, and cross-border e-commerce platforms in the United States have maintained historically low inventory levels in the first half of 2026. To prepare for the upcoming US Independence Day holiday consumption peak and the traditional autumn and winter sales season, American merchants have launched large-scale centralized restocking plans since April, generating massive cross-border cargo transportation demands for Chinese manufacturing goods.

China’s complete industrial chain and stable supply chain advantages have further amplified trans-Pacific cargo volumes. Affected by the uncertainty of global trade policies and fluctuating production costs in Southeast Asian manufacturing bases, a large number of export orders that previously shifted to Southeast Asia have returned to China in 2026. Electronic products, household appliances, textile products, and daily consumer goods, which are core advantageous export categories of China, have seen a sharp increase in export volumes to the United States, continuously squeezing the limited cabin space of trans-Pacific routes.

Industry logistics data shows that the cargo volume of China-US trans-Pacific routes increased by more than 35% month-on-month in May 2026, far exceeding the average monthly growth rate of off-season cargo volumes in previous years. The concentrated release of restocking demands has led to a rapid shift of the trans-Pacific shipping market from a balanced market to a seller’s market. Shipping carriers have taken the opportunity to adjust freight rates multiple times, and the market has formed a strong expectation of continuous price increases. Many exporters choose to book cabins in advance to lock in shipping costs, which further intensifies cabin shortages and pushes freight rates to rise rapidly.

In addition, the steady recovery of US consumer confidence has boosted terminal market purchasing power. The continuous growth of offline physical retail and online e-commerce orders has formed a superposition effect of commercial cargo and e-commerce parcel cargo, further expanding the cargo volume gap. Different from the single holiday-driven demand in previous years, this round of demand growth is based on the fundamental restocking needs of the US supply chain, with strong sustainability, laying a solid foundation for the continued tight operation of China-US shipping routes in the next one to two months.

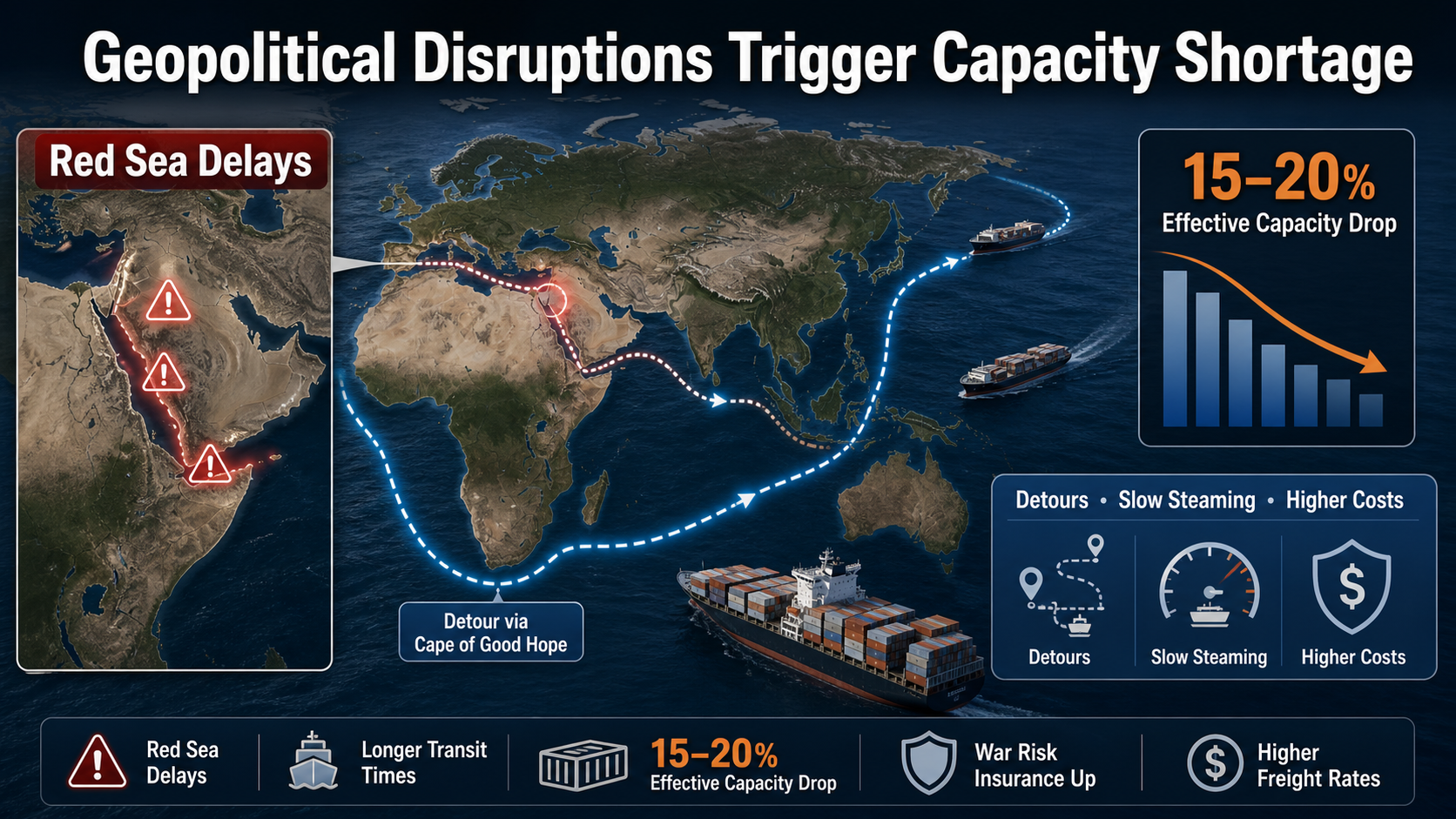

While market demand is rising steadily, severe supply-side capacity shrinkage is the key factor that exacerbates the imbalance of China-US shipping market. The continuous escalation of Middle East geopolitical conflicts and the delayed resumption of normal navigation in the Red Sea have brought unprecedented shocks to global container shipping capacity. According to industry statistics, more than 300,000 standard container capacities are currently stranded in the Persian Gulf region due to regional tensions, directly withdrawing a large number of effective capacities from the global trans-Pacific shipping market.

The delayed recovery of Red Sea navigation has become another major bottleneck restricting shipping capacity. Originally expected to resume normal navigation in the second quarter of 2026, Red Sea shipping routes have been repeatedly delayed due to continuous regional security risks. The vast majority of container vessels still have to take detours around the Cape of Good Hope instead of passing through the Red Sea and Suez Canal. This detour increases the single voyage distance by 7 to 14 days, greatly extending the shipping cycle of global container vessels. The prolonged voyage cycle directly reduces vessel turnover efficiency, and the limited number of vessels can complete fewer transportation tasks within the same cycle, which is equivalent to a substantial reduction in market effective supply.

Moreover, global shipping carriers have generally reduced vessel sailing speeds to cope with rising fuel costs and navigation risks, further squeezing effective shipping capacity. Slow steaming has become a common operation strategy for major shipping companies in 2026. Although this measure can reduce fuel consumption and navigation risk premiums, it further lowers vessel turnover efficiency and aggravates the market capacity gap. Industry analysis shows that the combined impact of Red Sea detours and slow steaming has reduced the overall effective capacity of global container shipping by 15% to 20% compared with normal levels.

The superimposed impact of rising operating costs also supports the high freight rate trend. Affected by global oil price fluctuations, marine fuel prices have risen sharply in 2026, bringing a substantial increase in fuel costs for shipping enterprises. At the same time, the geopolitical risks in the Middle East have led to a skyrocketing maritime war risk insurance premium, further increasing the comprehensive operating costs of trans-Pacific shipping. Major international shipping companies have successively issued freight rate increase notices since May, and the rigid cost increase has become an important support for the continuous rise of China-US shipping freight rates.

In terms of market operation, leading shipping companies have further controlled cabin supply by adjusting route layouts and suspending partial voyages to maintain freight rate stability. The top five global container shipping companies control more than 65% of the market capacity, with strong market pricing power. In the face of surging market demand and shrinking effective capacity, shipping carriers have no incentive to increase capacity significantly, and the tight supply pattern will continue.

Looking ahead to the market trend in the third quarter of 2026, industry insiders predict that the China-US shipping market will remain in a state of tight supply and high freight rates in the short term. On the demand side, the US pre-holiday restocking cycle will continue until August, and the continuous release of export orders will keep cargo volumes at a high level. On the supply side, the Red Sea navigation recovery progress is still uncertain, the Middle East geopolitical situation remains volatile, and the global effective shipping capacity is difficult to recover quickly.

For export enterprises and cross-border logistics practitioners, the next stage will still face challenges such as difficult cabin booking, high shipping costs, and easy container rollover. It is recommended that enterprises reasonably arrange shipment plans, book shipping spaces in advance, and flexibly adjust logistics strategies to cope with the continuous changes in the trans-Pacific shipping market. With the gradual easing of geopolitical risks and the adaptation of shipping capacity to market demand, the China-US shipping market is expected to gradually return to a stable state in the fourth quarter of 2026.

Email:

Email: